Huawei is making significant moves in the energy sector. On March 26, 2025, the Huawei China Digital Energy Partner Conference took place, where Huawei introduced three core strategies: the integration of solar energy, storage, and charging is becoming an inevitable trend, the launch of a native solar storage and charging solution; liquid cooling charging solutions targeting commercial vehicles; and the establishment of a supercharging alliance to seize opportunities in the national supercharging network.

Many are unaware that Huawei Digital Energy, as a key part of Huawei’s business, generates over 50 billion yuan in revenue annually, with numerous projects both domestically and internationally featuring Huawei’s involvement. Currently, Huawei’s primary focus in the energy sector is the integration of solar energy, storage, and charging, driven by these three strategic initiatives.

According to the China Industrial Research Institute in its report titled “Development Status and Investment Trend Forecast of China’s Solar Energy, Storage, and Charging Integration Industry (2025-2030)“, the global solar energy, storage, and charging market exceeded 65 billion yuan in 2023, with China holding a dominant 51.09% of the global market share. By 2025, the market size in China is projected to reach 113.42 billion yuan, indicating rapid growth.

This industry, which spans across solar power, batteries, and energy storage, has attracted major players like Huawei, BYD, CATL, along with numerous solar energy giants, paving the way for companies like Shouhang New Energy that are on the verge of going public. It seems this market is poised for explosive growth.

What is the Rising Trend of Solar Energy, Storage, and Charging Integration?

Solar energy, storage, and charging integration, as the name suggests, involves constructing solar power generation, energy storage systems, and charging facilities together, creating a large charging station. For instance, in the context of charging electric vehicles, solar panels atop the charging station convert sunlight into electricity, supplying power to charging piles and energy storage facilities while enabling commercial operations.

In fact, the State Council introduced the “New Energy Vehicle Industry Development Plan (2021-2035)” in 2020, which emphasized the coordination of energy utilization for new energy vehicles with wind and solar energy generation, encouraging the establishment of multifunctional integrated stations for “solar energy storage and charging”.

So why are external stakeholders only recently witnessing major announcements from giants like Huawei? There are two main reasons:

- Firstly, while the top-level planning was initiated early, the related industries depend heavily on specific policy support. The construction policies for solar energy, storage, and charging integration projects in various regions have only recently caught up, such as Shanghai’s release of the “New Energy Storage Demonstration Leading Innovative Development Work Plan (2025-2030)” at the beginning of the year. It is well-known that subsidies are a key driving force for development in the energy sector.

- Secondly, the achievements of these giants often come after years of cultivation in the industry chain, where they begin to consolidate their business models, leading to the latest changes. A solar energy, storage, and charging integrated station involves technologies in charging, battery, solar power, and smart management.

This brings us to a crucial question: which giants are behind the integration of solar energy, storage, and charging?

The first group is primarily vertical energy companies. Examples include solar power firms like Trina Solar, Sungrow Power, JA Solar, and LONGi Green Energy, battery leader CATL, and emerging companies specializing in solar and storage solutions like Shouhang New Energy, which is set to go public soon. In February, LONGi Green Energy emphasized the integration of solar energy and storage at a promotion meeting in Shandong, aiming to surpass the traditional combination of solar and storage.

However, it’s clear that one of the end goals of solar energy and storage integration is to generate revenue from electricity sales. The incorporation of the “charging” segment makes the business model more complete. Thus, companies like Huawei, which represent a second group of cross-industry and scenario-based service enterprises, are stirring up greater changes.

The Disruptive New Forces

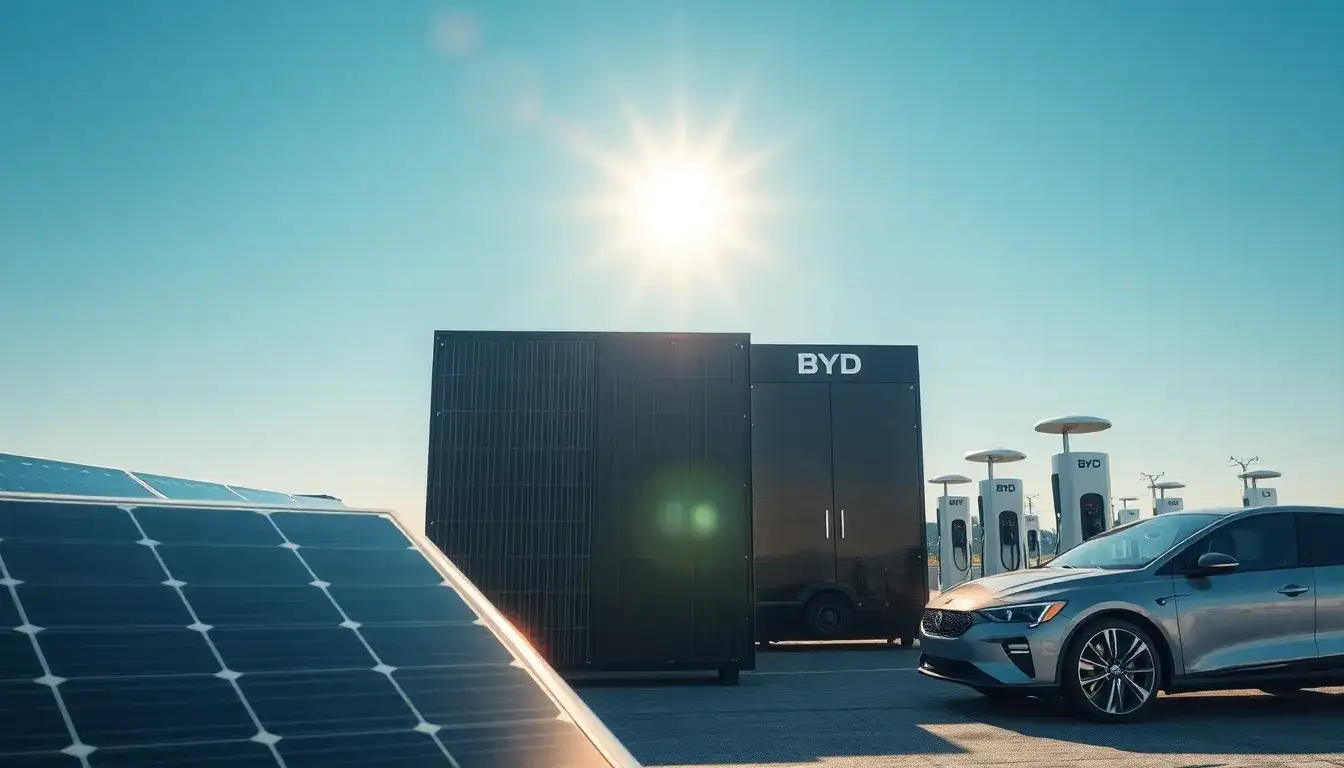

The second group consists of “ecosystem” companies—those that supply solar energy, storage, and charging products while also engaging in operational services. Companies like Huawei, BYD, Star Charge, and Telai Electric are included in this group. However, Huawei remains the most representative player, having been involved in the solar energy and storage charging sector for over a decade.

Huawei Digital Energy’s three strategies clearly stem from the perspective of solar energy, storage, and charging integration, aiming to occupy the best ecological position. This may come as a surprise, as Huawei emphasizes its non-automotive focus in the new energy sector, yet it is fully engaged in everything from infrastructure to supercharging construction.

At the end of the last century, when Huawei first emerged, it recognized the high power requirements of telecommunications equipment, which market suppliers could not meet. Therefore, it chose to manufacture its own power supplies and became the largest domestic telecommunications power supplier by 2000. Unfortunately, the subsequent internet bubble burst impacted telecommunications market demand, leading Huawei to sell its electrical business. It wasn’t until around 2010 that the global solar photovoltaic industry began to flourish. Huawei, having previously exited the energy sector, found that its technical expertise in power management and equipment aligned perfectly with the solar photovoltaic market, particularly in inverters, prompting its re-entry into the energy market and establishing a comprehensive solar energy, storage, and charging integration layout.

Through these ups and downs, it is evident that energy has always been a highly valued business for Huawei, which has never given up on it over the years. According to Huawei’s annual report, the digital energy business achieved 52.6 billion yuan in revenue in 2023, nearly on par with its cloud computing business.

In comparison, BYD, which primarily focuses on new energy vehicles, has also emerged as an invisible giant in solar energy, storage, and charging. On March 24, BYD released its 2024 annual report indicating substantial growth in its clean energy businesses, including energy storage, solar energy, and secondary charging batteries. Although the scale of its solar energy and storage business is not large compared to the automotive segment, which accounts for 79.45% of its business, BYD’s strong foundation in the automotive market significantly benefits its expansion into energy.

Both Huawei and BYD share common traits, indicating why these seemingly “outsider” giants can influence the solar energy, storage, and charging landscape.

- Firstly, they have tapped into the enormous demand pool of the automotive industry, bringing them closer to applications like charging stations. Particularly, if their developments in supercharging technology succeed, they will gain control over relevant standards and enhance their competitiveness in solar energy and storage integration.

- Secondly, the solar energy and storage industry relies heavily on the supply chain, and currently, there is an oversupply of domestic photovoltaic storage capacity at low costs. Traditional energy companies can enter the solar energy, storage, and charging integration market with minimal pain, especially for cash-rich companies like Huawei.

- Thirdly, both companies originated from the manufacturing industry and possess strong R&D capabilities. For instance, Huawei leveraged its early research in telecommunications power supply to enter the solar inverter market, quickly moving away from traditional centralized inverters to develop a more reliable “string architecture with intelligent management” model, securing the largest market share globally. The world’s largest solar energy storage microgrid built by Huawei in Saudi Arabia employs its own intelligent string inverters, smart string storage units, and proprietary electrochemical storage systems.

Lastly, Huawei’s sales capabilities are noteworthy. In 2015, when the news broke that China Minmetals was to build the world’s largest photovoltaic power station in Ningxia, Huawei’s sales team quickly engaged with China Minmetals for in-depth communication and secured the client.

The Solar Energy, Storage, and Charging Market is Entering a Competitive Phase

Undoubtedly, companies like Huawei and BYD are already equipped to reshape the future of solar energy, storage, and charging integration and even alter the energy market landscape. The current domestic environment favoring new energy further empowers them.

Previously, most people might not have heard of solar energy, storage, and charging integration, as early market demand primarily did not target individuals. Nowadays, while corporate and government layouts still dominate, the significant variable of new energy vehicles is aggressively seizing opportunities for solar energy, storage, and charging integration.

Last year, Huawei Digital Energy revealed that by the end of 2023, over 3.3 million households had opted for Huawei’s home solutions. At the recent conference, Huawei Digital Energy explicitly stated: “By collaborating on solar energy and storage, we can reduce electricity costs by 30% and achieve 100% local consumption of solar energy, ensuring quality charging wherever there are roads.”

Behind this development lie two significant industry trends, signaling the arrival of another competitive phase. The competition in solar energy, storage, and charging integration may rival that of new energy vehicles.

The first trend is the shift in market focus. Both traditional energy companies and players like Huawei were previously more active overseas. For example, JA Solar secured the position of preferred supplier for the largest solar energy storage project in the UAE, while BYD won a power project bid in Saudi Arabia early this year, breaking records for Chinese companies’ overseas storage orders. They now aim to create phenomenon products similar to their blade batteries and Han series, striving for the top share in the global storage market. This shift is primarily due to domestic energy companies having not yet entered a period of intensive solar energy, storage, and charging construction, while overseas demand for household storage is robust, presenting better profit margins than the domestic market.

However, as domestic penetration of new energy vehicles increases and policies encouraging solar energy, storage, and charging integration become clearer, companies are redirecting their efforts back home to seize these opportunities. In May of last year, the first integrated low-carbon service area in Hainan featuring solar energy, storage, and charging was unveiled in Sanya, with Huawei as the solution provider. Huawei’s intelligent solar energy storage solutions and all-liquid cooling supercharging technology are currently being promoted nationwide.

The second trend indicates that with the expansion of solar energy, storage, and charging, managing energy effectively will require increasingly sophisticated intelligent capabilities. What sets Huawei apart is its comprehensive intelligent technology that spans the entire chain from power generation to terminal charging facilities. For instance, Huawei’s intelligent solar and wind storage generator can achieve high levels of automation and stable operation in power plants, while its first globally developed intelligent string storage platform can reduce the cost per kilowatt-hour and enhance safety monitoring capabilities through sensors.

Moreover, as this segment grows, the ways enterprises enter the market are diversifying. In terms of capital, companies like Xiaomi and its founder Lei Jun are extensively entering the storage, battery, materials, and solar energy sectors through investment institutions, with over 20 recorded investments since 2022. Last year, Xiaomi also became a new shareholder of Keda Intelligent, a storage company actively pursuing modular storage and microgrid control technology to achieve solar energy, storage, and charging integration.

Clearly, with more players entering the market, solar energy, storage, and charging integration is set to become the next market hotspot. As it enters a competitive phase, the scenes previously witnessed in the photovoltaic, storage, and new energy vehicle sectors are likely to reoccur in this intersecting and complex field.